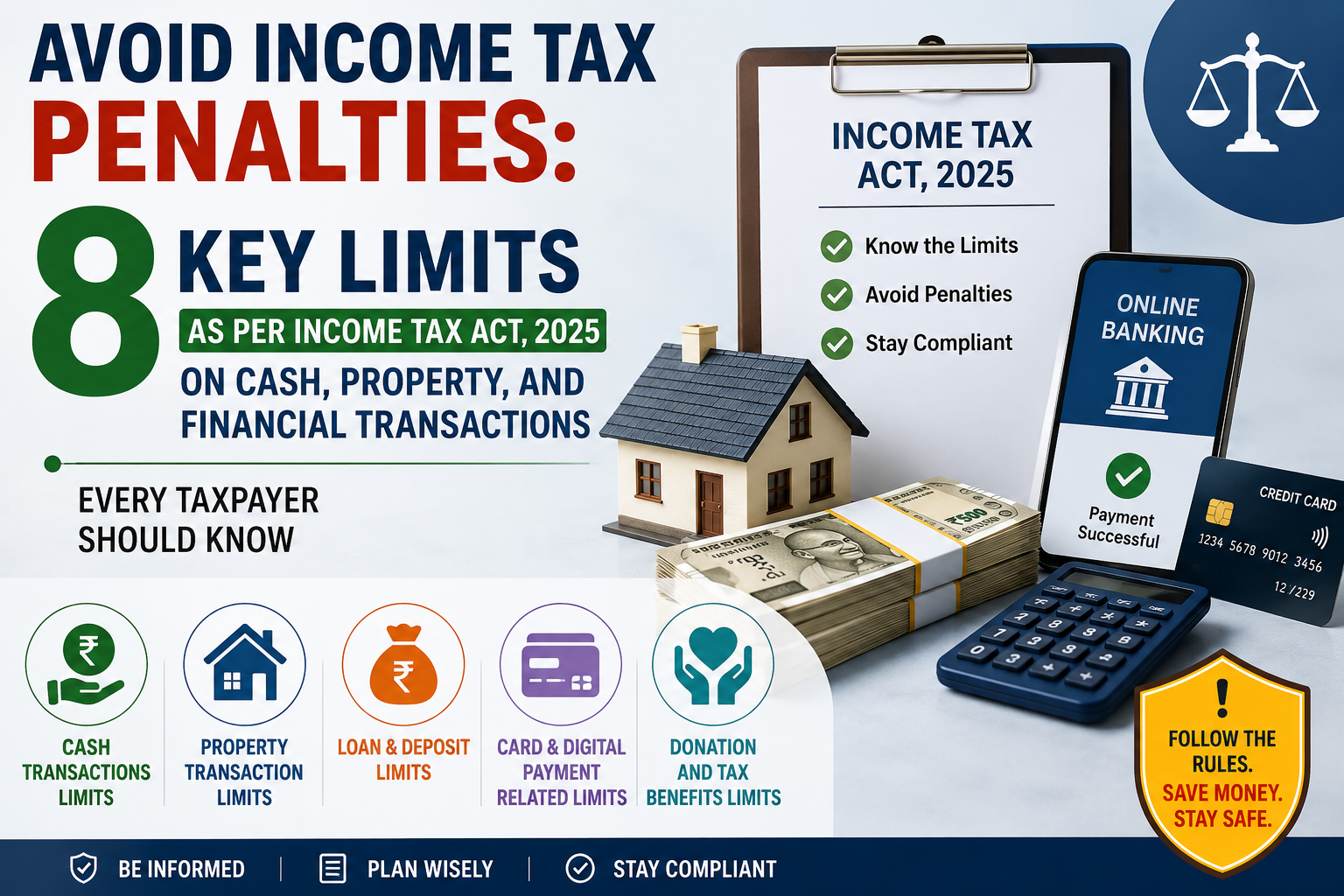

While filing your Income Tax Return (ITR) on time is essential, complying with the Income Tax Act, 2025 goes far beyond meeting the filing deadline. The law sets specific limits on various cash transactions—including cash receipts, loans, repayments, business expenses, donations, and property dealings—to improve financial transparency and discourage tax evasion. Breaching these limits can lead to penalties, disallowance of deductions, or increased scrutiny from the Income Tax Department.

To help taxpayers stay in compliance with tax law, Abhishek Soni, CEO & Co-founder of Tax2win and a Chartered Accountant, outlined eight key income tax transaction limits every taxpayer should know. Whether you are a salaried individual, business owner, investor, or property buyer, understanding these provisions can help you avoid unnecessary tax notices, penalties, and compliance issues.

8 Important Income Tax Limits Every Taxpayer Should Know to Avoid Penalties

1. Avoid Receiving ₹2 Lakh or More in Cash

The Income Tax Act, 2025 places a strict restriction on receiving ₹2 lakh or more in cash to promote transparency and discourage the use of unaccounted money. This restriction applies when:

- From a single person in a single day

- For a single transaction, regardless of the number of instalments

- For transactions relating to one event or occasion from the same person

For instance, if you sell goods or provide services and receive ₹2.5 lakh in cash, or accept the same amount as payment for a wedding, celebration, or any other event, the transaction may violate the law. Splitting the payment into smaller cash instalments does not bypass the restriction if it relates to the same transaction or occasion.

Penalty: If this provision is violated, the tax authorities may impose a penalty equal to the entire amount received in cash, making compliance with this rule essential.

2. Avoid Accepting Cash Loans or Deposits of ₹20,000 or More

The Income Tax Act, 2025 prohibits the acceptance of cash loans, deposits, or specified sums of ₹20,000 or more. The objective of this provision is to promote transparent financial transactions and reduce the circulation of unaccounted cash by encouraging the use of banking channels such as bank transfers, cheques, or demand drafts.

This rule also covers cash advances received for property transactions, including a house, apartment, or plot. Even if the property deal is not ultimately completed, accepting the advance in cash beyond the prescribed limit can still result in a violation of the law.

Example – if you get a loan of ₹30,000 from a person or accept a cash booking advance of more than ₹20,000 for the sale of a property, the transaction may attract the attention of the Income Tax Department and lead to penal action.

Penalty: If you violate this provision, the tax authorities may levy a penalty equal to the amount of the loan, deposit, or specified sum accepted in cash.

3. Avoid Repaying Loans or Deposits of ₹20,000 or More in Cash

The Income Tax Act, 2025, not only restricts the acceptance of large cash loans and deposits but also places limits on their repayment. If you repay a loan, deposit, or specified advance of ₹20,000 or more in cash, the transaction may be treated as a violation of the Act. To ensure transparency and maintain a proper audit trail, such repayments should be made through banking channels or other prescribed electronic payment modes.

This provision applies to loans, deposits, and certain advances, including those related to immovable property transactions. For example, if you repay a cash loan of ₹25,000 or return a property-related advance of ₹20,000 or more in cash instead of through a bank transfer, cheque, or other permitted mode, you may attract penal action under the Income Tax Act.

Penalty: If this provision is violated, the tax authorities may impose a penalty equal to the amount repaid in cash.

4. Business Cash Payments Above ₹10,000 May Not Qualify for Tax Deduction

The Income Tax Act, 2025 discourages businesses from making large cash payments by restricting the tax deduction available on such expenses. If a business makes a cash payment exceeding ₹10,000 to a single person in one day, the expenditure is generally not allowed as a deductible business expense while computing taxable income. This particular rule facilitates businesses to use bank transfers or other approved digital payment methods for better transparency.

For example, if a business pays ₹15,000 in cash to a supplier for the purchase of goods or services in a single day, it may not be able to claim that amount as a business expense. As a result, the taxable income of the business could increase, leading to a higher tax liability.

Exception: A higher threshold applies to businesses engaged in the business of plying, hiring, or leasing goods carriages. In such cases, cash payments of up to

5. Make Donations Above ₹2,000 Through Digital Modes to Claim Tax Benefits

The Income Tax Act, 2025, encourages taxpayers to make charitable donations through traceable payment methods rather than cash. If you make a cash donation exceeding ₹2,000, you cannot claim a tax deduction for that contribution under the applicable provisions relating to charitable donations, even if the donation is made to an eligible institution or charitable organisation.

For instance, if you donate ₹5,000 in cash to a registered charitable trust, you will not be entitled to claim a tax benefit on that amount. However, if the same donation is made through a recognised banking or digital payment channel, you may be eligible to claim the deduction, subject to the conditions prescribed under the Income Tax Act.

To avail of tax benefits on eligible donations, it is advisable to make the payment through one of the following modes:

- UPI

- Net banking

- Cheque

- Demand draft

- Other prescribed electronic payment methods

Using these payment methods not only helps you claim the eligible tax deduction but also creates a proper transaction record for future reference

6. Large Cash Withdrawals May Attract Higher TDS

The Income Tax Act, 2025, does not prohibit individuals from withdrawing their own money from bank accounts. However, if you withdraw large amounts of cash and meet certain conditions under the Income Tax Act, the bank may deduct Tax Deducted at Source (TDS). The government introduced this provision to discourage excessive cash transactions and promote the use of banking and digital payment channels.

The TDS rules are particularly relevant for taxpayers who have not filed their income tax returns for the prescribed period. If such individuals withdraw cash beyond the notified threshold from a bank, co-operative bank, or post office, the institution may deduct TDS before releasing the funds. This can affect cash flow, even though the money belongs to the account holder.

For example, a person who has not complied with the return filing requirements and makes large cash withdrawals during the financial year may face a higher TDS deduction as prescribed under the Income Tax Act.

Tip: Filing your income tax returns regularly and on time can help you avoid higher TDS on cash withdrawals and ensure smoother access to your funds.

7. Avoid Using Large Cash Payments in Property Transactions

The Income Tax Act, 2025 discourages the use of cash in property transactions to improve transparency and curb the circulation of unaccounted money. Under the law, you cannot receive or pay ₹20,000 or more in cash for buying or selling a house, flat, plot, or any other immovable property.

For example, if a buyer pays a property booking amount or advance of ₹20,000 or more in cash, the transaction may violate the provisions of the Income Tax Act and could attract penal consequences. Such transactions may also draw the attention of the Income Tax Department, increasing the likelihood of scrutiny or further verification.

To avoid compliance issues and maintain a clear audit trail, experts recommend making all property-related payments—including booking advances, instalments, and the final consideration—through bank transfers, account payee cheques, demand drafts, or other prescribed electronic payment methods.

8. Splitting Large Cash Transactions Will Not Help You Bypass the Rules

Some taxpayers believe they can avoid the cash transaction limits under the Income Tax Act by dividing a large payment into multiple smaller cash payments. However, the law specifically prevents such practices and considers the overall nature of the transaction rather than just the individual payment amounts.

The prescribed limits apply to:

- Total cash received from the same person in a single day

- Multiple cash payments made for a single transaction

- Payments relating to one event or occasion, even if made in instalments

For example, receiving several smaller cash payments for the same property deal, business transaction, or event does not exempt you from the provisions of the Income Tax Act. If the combined amount exceeds the prescribed limit, you may violate the Income Tax Act.

Attempting to artificially split cash transactions does not help avoid compliance requirements. Instead, it may invite scrutiny from the Income Tax Department and expose taxpayers to penalties. To stay compliant, it is advisable to use banking channels or prescribed electronic payment methods for high-value transactions.

FAQs

Q1. Is it permissible to accept a cash loan of ₹25,000 from a friend?

Ans. No. Under the Income Tax Act, you cannot accept a cash loan of ₹20,000 or more. If you do, you may violate the law and face a penalty equal to the amount you accepted in cash.

Q2. Can I claim a tax benefit on a ₹5,000 donation made in cash?

Ans. No. Donations made in cash exceeding ₹2,000 do not qualify for a tax deduction under the Income Tax Act. To claim the eligible tax benefit, make the donation through approved banking or electronic payment modes.